Martin Lewis Warning: Why Saving Your Money Could Be Making You Poorer (Investing vs. Saving)

- May 1

- 4 min read

Is your savings account a trap? Martin Lewis explains why £1,000 in savings actually lost value over 10 years compared to investing. Learn how to beat inflation and start your journey from Grad Rags to Riches.

Investing vs. Saving: The 10-Year Reality Check

In a recent podcast, the UK’s favourite money mentor, Martin Lewis, dropped a financial "bomb." His concern isn't that we aren't putting money away, it’s that we’re putting it in the wrong place.

If you are looking to build long-term wealth, understanding the "scale of magnitude" between cash and the stock market is the difference between treading water and actually getting ahead. Here is what the great man had to say:

The 10-Year Showdown: Savings vs. Investing

“When we ask for questions on savings and investments, the vast majority of questions are about savings, not investment. That worries me.

We talked earlier in the show about investing. Now, on the balance of probabilities, if you invest in a broad spread of assets over the long run, investments are likely to grow significantly faster than savings. Significantly, many times faster.

Some actual numbers for you...we're going to look at a 10-year period up until the end of last year.

We're going to assume that if you had savings, you kept the interest in the account so that compounded, and if you put it in a fund, then any dividends, that's the income you make on shares and funds, were also reinvested and bought you more shares, so they compounded too.

It's worth noting this particular period we're looking at was a low-interest rate period, so the savings returns were particularly low...but still, in contrast, this is a long 10-year period just to show you the difference.

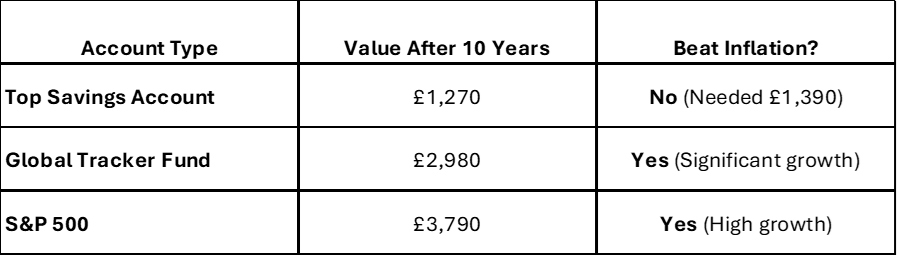

So, if you had put £1,000 in savings at the start, at the end, you would have made £270. In other words, you would have got £1,270 back.

But just to keep up with inflation, you would have needed to get £390 back… in other words, you didn't keep up with inflation. So, in real terms, by putting your money in the savings, and these were the top savings it was calculated upon…you would have still actually seen your purchasing power diminished.

You would not have had enough in the account after 10 years with £1,270 to buy what £1,000 would have bought you when you first put it in.

Now, let's contrast that to a couple of different tracker fund investment options. If you had put the £1,000 in a global tracker and had the dividends reinvested, by the end of the 10 years, you would have made £1,980. In other words, you'd have got £2,980 back.

A massive difference, far above inflation and smacking the pants off savings. If you'd gone to put it in the S&P 500, which is the top 500 US biggest shares… then you would have got £3,790 back”.

Source: The Martin Lewis Podcast

The Scenario: £1,000 Initial Deposit

If you had put £1,000 away a decade ago, here is what that money would look like today:

The Verdict: While the savings account grew, its purchasing power diminished. You would not have enough in that account today to buy what £1,000 could have bought you ten years ago.

Now, of course, as you're supposed to say, and as is absolutely true, past performance is no indicator of future performance, so there are no guarantees this would happen again. But Martin Lewis has shown the scale of magnitude of placing money in a low-cost global index fund, compared to a savings account over those 10 years.

5 Reasons You Should Love Index Investing

At Grad Rags to Riches, we advocate for "passive" or index investing. Here is why it’s a game-changer:

It’s Simple: Use low-cost global funds to keep your "eggs in many baskets" without trying to time the market.

It Works: Study after study shows that index funds beat the majority of actively managed funds over the long term.

It’s Affordable: You can start with small, regular chunks and build your portfolio slowly.

It Saves Time: No need to pore over company accounts or complex charts; you’re free to "sniff the roses".

It Puts You in Control: With a bit of confidence and self-education, you can manage it yourself, which means you avoid paying hefty commissions or advisor fees.

Should you invest?

Before you think about investing, you'll want to make sure you’ve got all your other ducks in a row first.

That means doing things like paying off high-interest debt, and making sure you have emergency funds somewhere safe and accessible (Martin's nodding along).

Next, there are two big questions about whether it's time for you to invest with some or all of your assets, or not:

Is it money you don't need to access at the moment?

Is it money you're putting away for the long term, e.g., a minimum of five years?

If there is a nervousness that you don't want to put it all into a shares ISA, you can have both a cash ISA and a shares ISA, and you can put some in each.

If you've got a long timeline ahead of you – think five to 10 years at minimum to give you the best possible chance of riding out the market's ups and downs, investing has been the best way to build wealth and outrun inflation over the last century.

As a Grad starting your wealth-building journey, the 'cost of waiting' is your biggest enemy. Check out our YouTube playlist, Step-by-Step Guide to Becoming Wealthy to get started today.

Martin and gradragtoriches knows best!