What is an Innovative Finance ISA: 10% Returns v The Catch

- Apr 4

- 4 min read

Is a 10% return too good to be true? Explore the risks and rewards of Innovative Finance ISAs in 2026, including top providers like Loanpad and Kuflink.

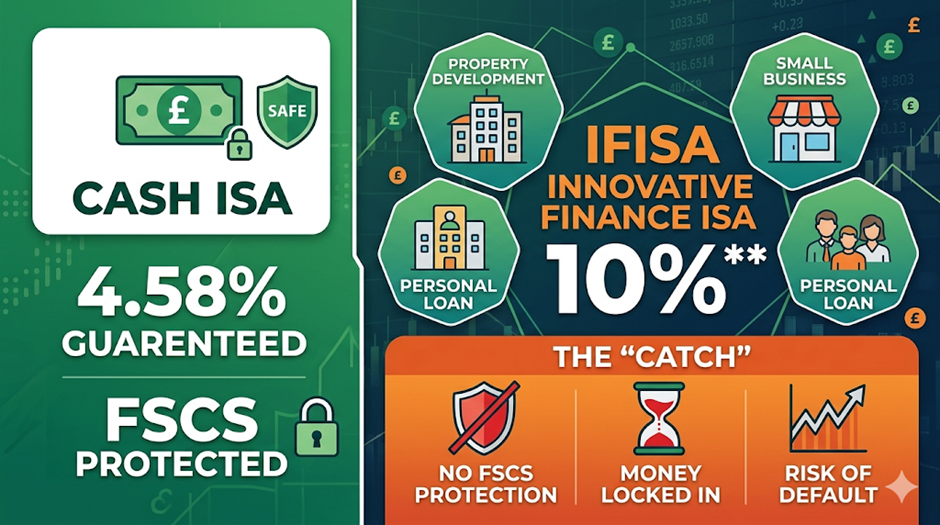

There is an ISA out there that currently claims to pay more than 10% a year completely tax-free. This sounds great and is exactly what you want to hear when you put your money to work. Compare this to the best cash ISA at the moment, where you can make a guaranteed 4.58%, and this becomes very attractive.

So, why aren't people talking about it and what's the catch that we're all missing?

The Secret ISA

An Innovative Finance ISA is a lesser-known form of tax-free savings account that allows you to invest in peer-to-peer lending or other forms of debt-based securities. In exchange, you can potentially earn higher interest rates than you would with a cash or stocks and shares ISA.

When you open an IFISA, you stop being a saver and start being a lender. You're lending your money through platforms that connect you to individuals or businesses seeking loans. These borrowers could be looking for personal loans, business loans, or property development funding.

In return for lending your money, you'll earn tax-free interest just like any other ISA, with the key advantages of potential returns of between 5% and 10%, which can be much higher than a typical cash ISA.

The highest easy access cash ISA currently is with Trading 212, offering 4.58% (includes a 0.98% 1year bonu

s). That’s a guaranteed return.

Notable IFISA Providers in 2026

While Funding Circle and other pioneers like RateSetter have exited the retail market, several specialist platforms still offer Innovative Finance ISAs as of 2026. These current providers often focus on niche markets such as property development, bridging loans, or green energy.

What happened to Funding Circle?

Funding Circle’s peer-to-peer operation was once the cornerstone of the UK’s "alternative finance" movement, allowing individual retail investors to lend directly to small businesses for attractive interest rates. However, the platform permanently closed to retail investors in March 2022.

The decision followed a two-year suspension of retail lending during the COVID-19 pandemic, during which the company pivoted toward government-backed loan schemes and institutional funding.

Management ultimately concluded that the retail P2P model was no longer commercially sustainable, citing the high costs of meeting increasingly stringent FCA regulations.

While investors didn't lose their money overnight, the secondary market was shuttered, meaning they could no longer sell their loans to other investors for a quick exit. Instead, customers became locked in, forced to wait for their remaining loans to naturally amortise through monthly repayments.

RateSetter, formerly one of the UK’s largest peer-to-peer lenders, was acquired by Metro Bank in September 2020 and subsequently closed its P2P operations.

The Catch: Why 10% Isn't Free Money?

1. No FSCS Protection

Unlike a Cash ISA, which protects up to £120,000 via the Financial Services Compensation Scheme (FSCS), an IFISA has no such guarantee. If the borrower defaults or the platform collapses, you could lose 100% of your investment, or just get an extremely low return.

Although the companies operating these ISA’s are regulated and registered with HMRC, they're not offering you any guarantee or any protections in case the worst were to happen; it's really up to the provider to do all of the due diligence and make sure that they lend out your money to the right people who are more likely to pay back these loans.

2. The Liquidity Trap

Money invested using the IF ISA is not as liquid as cash or even stocks and shares. Buying and selling shares or ETFs is extremely easy these days. You can just open up your investing app and sell your shares as and when you want and get cash back in your bank account within one or two days.

Many IF ISAs have locked-in terms, and accessing money quickly can be difficult, as you must often wait for a loan to be repaid or for another investor to "buy you out". There is also a possibility that borrowers will be unable to repay their loans.

3. "Target" vs. "Guaranteed"

A Cash ISA rate is a guarantee. An IF ISA rate is a target, and unless they specifically state otherwise, there are no guarantees on what you could receive. If borrowers pay late or default, your actual return may be lower than the headline 10%.

Is an IF ISA right for you?

An Innovative Finance ISA is a "middle ground" asset. It offers higher yields than cash without the daily price volatility of the stock market.

If you're comfortable with taking on more risk and understand how peer-to-peer lending works, it can offer higher potential returns than a cash ISA.

It can be a good way to diversify investments across different types of loans. Since some of those loans have longer repayment periods, an IF ISA is better suited to those who can comfortably lock their money away for the medium to long term rather than those needing immediate access to their savings.

P2P lending provides exposure to alternative asset classes that do not correlate directly with stock market volatility. Many current providers focus on secured lending (e.g., property), providing a safety margin if the borrower defaults.

While the potential for higher returns is attractive, it's important to understand the risks associated. Unlike a traditional savings account, the money isn't protected by the Financial Services Compensation Scheme. This means if the lending platform or borrower fails, you may lose your investment, and there's no guarantee of compensation.

Just remember, an Innovative Finance ISA is not as safe as a traditional cash ISA. So, make sure you understand the platform you're using and the risks involved before committing.

Interesting thanks gradragtoriches